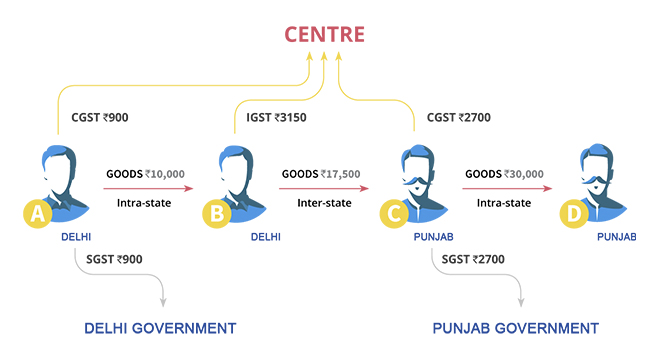

GST is a consumption based tax i.e. the tax should be received by the state in which the goods or services are consumed and not by the state in which such goods are manufactured. IGST will ensure seamless flow of input tax credit between inter-state movements of goods. One state has to deal only with the Center government to settle the tax amounts and not with every other state, thus making the process easier. For example: A dealer in Punjab sold goods to the consumer in Punjab worth Rs. 10,000. The GST rate is 12% comprising of CGST rate of 6% and SGST rate of 6%, in such case the dealer collects Rs. 1200 and Rs. 600 will go to the central government and Rs. 600 will go to the Punjab government. Now, if the dealer in Punjab had sold goods to a dealer in Delhi worth Rs. 1, 00,000. The GST rate is 12% comprising of CGST rate of 6% and SGST rate of 6%. In such case the dealer has to charge Rs. 12,000 as IGST. This IGST will go to the Center.

WHAT IS GST ?

| CGST | SGST | IGST | |

|---|---|---|---|

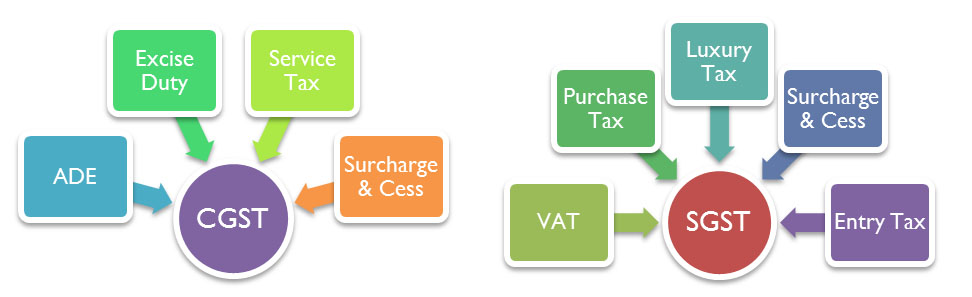

| Meaning | CGST means Central goods and service tax to replace the existing tax like service tax, excise, etc. and It is levied by Central Government | SGST means State goods and service tax, replace the existing tax like sales tax, luxury tax, entry tax, etc. and it is levied by the State Government | IGST refers to the integrated goods and services tax and it is a combined form of CGST and IGST and it is levied by Central Government |

| Collection of tax | Central Government | State Government | Central Government |

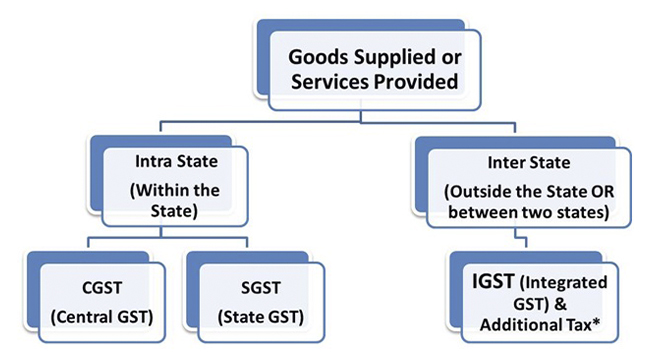

| Applicability | Intra-State supply | Intra-State supply | Inter-state supply |

| Registration | No registration till the turnover crosses 20 lakhs ( 10 lakh for north eastern states) | No registration till the turnover crosses 20 lakhs ( 10 lakh for north eastern states) | Registration is mandatory |

| Composition | The dealer can use the benefit up to 75 lakhs under the composition scheme | The dealer can use the benefit up to 75 lakhs under the composition scheme | The composition scheme is not applicable in inter-state supply |

Fundamentally every industry is likely to get benefit from GST as it will make the overall process of taxation simpler, less bureaucratic and efficient, out of which one industry shall be Transport & Logistics. Since long back, this industry had been attracting various types oflevies due to inter-state logistic structure based on the state taxation system which made it inefficient and clumsy. The Indian transport and logistics sector is primarily categorized into various segments consisting of transportation, warehousing, freight forwarding, pool distribution, packaging solutions, inventory management, management consulting, logistics optimization, etc…

| Service | Old | GST | Difference |

|---|---|---|---|

| Non AC Rail Ticket | 0 | 0 | 0 |

| AC Rail Ticket | 4.5 | 5 | +0.5 |

| Transporting goods by train | 4.5 | 5 | +0.5 |

| Transporting goods by truck | 4.5 | 5 | +0.5 |

| Tour operator | 9 | 5 | -4 |

| Cab service | 6 | 5 | -1 |

| Air Economy | 6 | 5 | -1 |

| Air Business | 6 | 12 | +3 |

Service tax is not applicable on the transport of the following goods:

- Relief material for disaster struck areas (food for flood victims etc.)

- Defense or military equipment

- Newspaper or magazines registered with the Registrar of Newspapers

- Railway equipment or materials

- Agricultural produce

- Milk, salt and food grain including flours, pulses and rice

- Organic manure

As proposed under GST, movement of goods worth more than Rs 50,000 within or outside a state will require applying for an E-Bill through online registration of the consignment. Tax officials are empowered to verify the validity and accuracy of the E-Bill to avoid tax evasion. Though the intent seems to be good, but due to process of multi-layered declaration it may prove to be cumbersome.

- In relation to a supply; or

- For reasons other than supply; or

- Due to inward supply from an unregistered person,

Every registered person who causes movement of goods of consignment value (consignment value > Rs. 50000/-) Exceeding fifty thousand rupees —

Before commencement of such movement, furnish information relating to the said goods in Part A of FORM GST EWB-01, electronically, on the common portal.

| Sr. no. | Distance | Validity period |

|---|---|---|

| (1) | (2) | (3) |

| 1. | Less than 100 km | One day |

| 2. | 100 km or more but less than 300km | Three days |

| 3. | 300 km or more but less than 500km | Five days |

| 4. | 500 km or more but less than 1000km | Ten days |

| 5. | 1000 km or more | Fifteen days |